As long as your conclusion is that China's GDP will keep growing at the government set pace, none of your arguments has substance. It's like complaining about the food at a restaurant while eating there every day.

If you wanna debate about something, then you need to set out the precise negative consequences that you expect to see on the Chinese GDP in a well-defined span of time, and it should be very near-term because nobody wants to go on a 20 year imagination journey with you.

There was a company in easter europe in the 80s ( actually there was countless fo them like it) that manufactured hundreds of expensive equipment for a customer.

But there was a flop in the quality of them, so they had to store all of them in the back yard.

This was finished goods, so all work/material was accounted like if they sold it, and it shown in the GDP number as manufactured item.

However in the 90s the liquidator of the company simply forked all euipment to the scrap yard.

So, what was the return on the investment on these machiens?

Example Pettis talking exaclty about this.

IF the driver of the growth is investment, then in the late phase ( where is China now) it is very hard to move all of the money into projects that has positive return.

It is easy to hide the losses under the rug ( the European banks are doing it with the greek goverment bonds, so it is not only Chinese speciality) nd book the machiens with full value, regardless if the liquidation value of it is the metal price

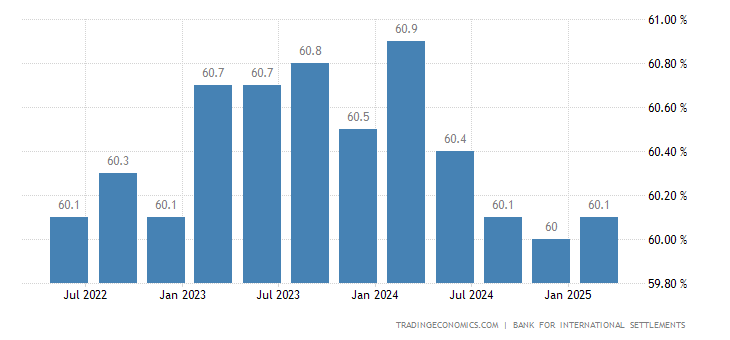

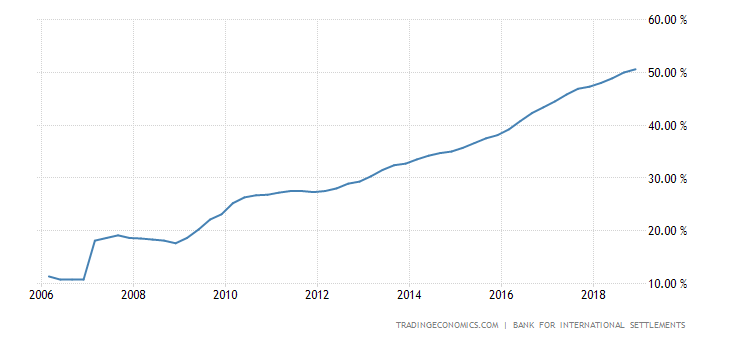

At the moment we don't know how big part fo the 60% investment/goverment/export activity hiding losses .

All that we know is the 40 % ish household consumption is extremly low, and if you use it as an indicator of the sustainable GDP number then there is at least 10 % loss in the headling GDP .

I have to remid you the GDP number important as a matter of national pride, but the household consumption can be used to buy food, shelter and cloth.

So the drop in the GDP doesn't metter , only the consumption important for the households.

In japan during the lost decades the consumption stayed as on level and slowly imporved, but all crazy investment/export business colapsed in slow motion.