I'm just trying to understand better China's refinery expansion, where they are getting oil from and what they are producing

Reading this, it's quite interesting to see how Middle Eastern exporters are directly getting connected with small private refineries. It's also interesting to read about the greenfield mega refineries. Quite interesting to see the toggle between Arabs, Russians and Iranians for business with China's independent refineries. A lot about liquids to chemical refineries makes me think that China is just ready to really take over the petrochemical market, especially with their access to low cost petroleum, advanced new refinery facilities and competitors facing high cost operation. Reading this, I think it will be good for the smaller refineries to be replaced by more modern refineries and to force exporters to trade over Shanghai energy exchanges.

China is now world's top refiner with a lot of new petrochemical capacity. Notice how the retired facilities are all in Shandong. Shandong is losing its place in China's refinery industries due to their facilities being older. Sounds like the entire industry is getting more efficient and older capacity are closed down. Interesting that even 77% in 2021 was an all time high for them and that those smaller shuttled facilities were running at 50% utilization. In America, I think the refineries in 2022 were running at over 90% utilization.

The end part is important too, because China's gasoline demand probably is flatlining due to the increasing EV presence, so they don't need to continue to increase their refining capacity for gasoline or even diesel. So, the additional refinery capacity could be exported or be used to increase their market share in petrochemicals. Probably why the new refineries are mostly liquids to chemicals plants.

Another good article here

China at 18.81 million bpd of refining in 2022 and looking to reach 20 million by 2025 with 80% utilization. Somehow, America is running at over 90% utilization with 17.7 million bpd of refining and continue to shutter its refinery capacity. With that kind of direction, America is clearly going to export less going forward.

The ESG commitment and demand is pushing all these energy companies to cut refineries in America and Europe. Great for the environment and not so much for energy security.

Reading this, it's quite interesting to see how Middle Eastern exporters are directly getting connected with small private refineries. It's also interesting to read about the greenfield mega refineries. Quite interesting to see the toggle between Arabs, Russians and Iranians for business with China's independent refineries. A lot about liquids to chemical refineries makes me think that China is just ready to really take over the petrochemical market, especially with their access to low cost petroleum, advanced new refinery facilities and competitors facing high cost operation. Reading this, I think it will be good for the smaller refineries to be replaced by more modern refineries and to force exporters to trade over Shanghai energy exchanges.

China is now world's top refiner with a lot of new petrochemical capacity. Notice how the retired facilities are all in Shandong. Shandong is losing its place in China's refinery industries due to their facilities being older. Sounds like the entire industry is getting more efficient and older capacity are closed down. Interesting that even 77% in 2021 was an all time high for them and that those smaller shuttled facilities were running at 50% utilization. In America, I think the refineries in 2022 were running at over 90% utilization.

The end part is important too, because China's gasoline demand probably is flatlining due to the increasing EV presence, so they don't need to continue to increase their refining capacity for gasoline or even diesel. So, the additional refinery capacity could be exported or be used to increase their market share in petrochemicals. Probably why the new refineries are mostly liquids to chemicals plants.

Another good article here

China at 18.81 million bpd of refining in 2022 and looking to reach 20 million by 2025 with 80% utilization. Somehow, America is running at over 90% utilization with 17.7 million bpd of refining and continue to shutter its refinery capacity. With that kind of direction, America is clearly going to export less going forward.

this is kind of crazy how much less refining capacity there are, especially in US and I don't think America has added any new refineries recently. This has caused diesel shortage big time.According to Biden, has shuttered since the beginning of the COVID pandemic, in the United States.

The ESG commitment and demand is pushing all these energy companies to cut refineries in America and Europe. Great for the environment and not so much for energy security.

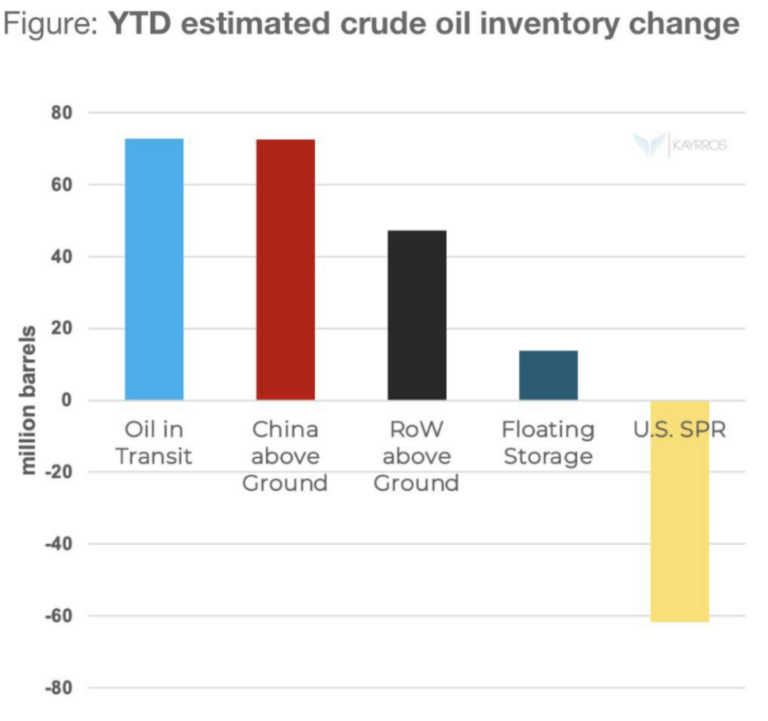

This picture of result of US SPR is quite enlightening. China is adding to its strategic reserve for a long time rather than refining more. As a result of this, it didn't export that much in the summer time and only started toward end of the year.Apparently, oil and gas companies and their investors have listened to policymakers’ calls for less investment in fossil fuels and have heeded those calls. For example, Shell operated , but cut the figure to 8 refineries to reduce the company’s climate footprint. By 2025, the company plans to operate 5 refineries.

Again, great for environment, but not great for energy security. While I expect America to have enough refining capacity for itself, I think its ability to export refined product to other Western countries on ESG commitment will continue to decrease over time. As such, we will like have China battling out with Middle Easterners and Indians for export to rest of the worldNo new major oil refinery has been built in the United States since the Carter administration and Biden’s climate policies and regulations will ensure that none are built in the future. Due to the renewable fuel standard and tax credits, some of the refineries that have not shuttered are being converted to biofuel facilities.

, the U.S. refining industry’s ability to respond to rising petroleum prices is definitely handicapped.